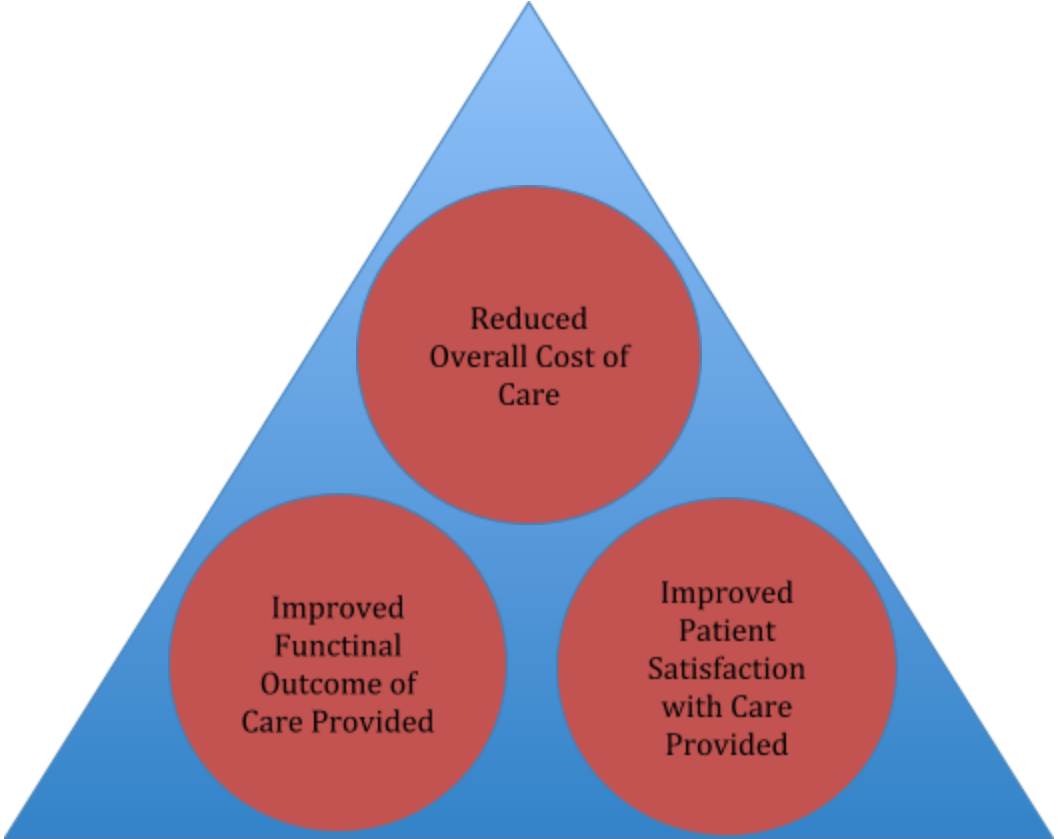

It has been 10 years now since the passage of the Patient Protection and Affordable Care Act (PPACA, AKA the ACA) in March 2010. In this period of time many provider groups have collaborated with many payer groups to achieve better healthcare. There certainly are proponents for and against this act, however one of the best aspects of this Act was the creation of the Triple-Aim:

The Triple-Aim

Who could argue against these goals?

Narrow Networks Defined

Almost 70 percent of all ACA plans have a limited, or narrow, range of providers/suppliers. This means they include 25 percent or less of the providers in the area. McKinsey & Company defines a narrow network as one containing 70 percent or less of the hospitals in a rating area. Providers and suppliers (O&P) will contract with payers at a more favorable rate in exchange for access to many enrollees. The more favorable rates can take the form of a traditional discount to an established fee schedule or other types of alternative payment models (APM’s) where providers/suppliers assume some risk with bundled or fixed rates. However, since the passage of the ACA a quality component has been added.

The Evolution of Plan Development

In the 10 years following, provider-payer partnerships have formed many different types of Accountable Care Organizations (ACO’s) including those referred to as Medicare Shared Savings Plans. Medicare established a list of both cost and quality benchmarks an organization has to meet or exceed in order to share in the savings created, in other words to get paid a bonus. Essentially these plans were allowed to establish their own benchmarks and then they were “graded” against these benchmarks. To establish the benchmarks the providers and payers had to look at their operational and clinical structure to ensure effective and efficient services relative to cost and quality partially measured by the patient via outcome measurement instruments. In the beginning not all of these ACO’s were profitable and some faded away and others kept refining their processes.

As time went on, not all provider groups were equal, and payers began to be selective in who participated in their plans. Payers recognized it is less expensive to retain an existing customer, employer group or individual, than it is to acquire a new customer, and providers recognized their ability to demonstrate cost and care effectiveness would also retain and attract new patients.

Thus, payers naturally began to narrow the provider panels to only those who could meet certain benchmarks. As payers and providers refined their processes, they became profitable in the ACA plans and are now beginning to move upstream in the Medicare Advantage plan market, which can be profitable.

Payers have moved from the low or no margin market of Medicaid Managed Care to the attractive ACA exchange plans. Now, in the early 2020’s payers are targeting the Medicare Advantage plans and they are bringing along their narrow networks of providers and suppliers and their data base or results.

Opponents will say limiting patient’s choice of providers will lead to poor and expensive care. However, consider this. How do we get better at doing anything? By doing more of it of course. Likewise, we reduce cost, by doing more of something. We learn how to refine processes, leverage technology, and manage supply chains better. It only makes sense for payers to limit the number of providers/suppliers their insureds can go to, while at the same time requiring their provider network to measure their results against a standard. This is more than pay to play, this is prove to play! Prove you can deliver the Triple-Aim and the world is your oyster.

According to the Kaiser Family Foundation, total Medicare Advantage enrollment was at its low in 2003-04 at 5.3 million. Total enrollments took off in 2006 at 6.8 million and have grown every year through 2019 with total enrollments at 22 million. This is 34 percent of all Medicare beneficiaries and this number is projected to grow to 47 percent by 2029. Just so happens this population also makes up the majority of prosthetic patients. To see where your state is click here. Interestingly, most of the Medicare Advantage plans are operated by three payers:

- UnitedHealthcare - 26 percent

- Humana - 18 percent

- BlueCross Blue Shield Affiliates - 15 percent

Three companies control 60 percent of a growing Medicare market. Also, of interest given the overall cost of O&P services, especially prosthetics, Medicare Advantage enrollees average out-of-pocket expenses are:

- $5,059 for in-network services

- $8,649 for in-network and out-of-network PPO services.

Along with a shift towards these Medicare Advantage programs is the requirement for prior authorizations by 80 percent of the Advantage plans. This is a concept the private payers have a great deal of experience with and Medicare is just now requiring on a limited basis for prosthetic services.

Not only are payers and provider groups changing the care landscape affecting how O&P will interface with them from a cost and quality standpoint, so too will technology affect who is an O&P player in the narrow network. The input of digital scanning and telemedicine combined with lower cost yet competent care extenders has the potential to change who provides what to whom, when, and at what cost. Does the traditional O&P model continue work moving forward?

The Focus on Quality Has Arrived

The upshot here is, the concept of narrow networks based on cost and quality are growing and Medicare Advantage plans are growing as well. The Kaiser Family Foundation also indicates 72 percent of Medicare Advantage enrollees are in plans receiving four-star (out of five) quality ratings and related bonus payments. O&P practices need to be cognizant of these changes and adapt accordingly to remain viable.

While O&P is not eligible for bonus payments, you can ensure you are part of the Narrow Network Club, so-to-speak, by being able to demonstrate your quality metrics through an objective patient-centered outcomes program. This is called an Evidence-Based Practice (EBP) approach, which I wrote about in a previous article. Among the benefits mentioned in this article, an EBP can add value to your operations in five critical ways:

-

Clinicians stay current with best practices

- Collecting data from your patients allow you to see in almost real time what is working and what is not relative to best practices.

-

Access to your data as it comes in

- Clinician’s time is valuable and there never seems to be enough time in the day especially with documentation demands being what they are. So how does one stay up to date with journal reviews? Also given published materials relative to the effectiveness of O&P has been questioned by policymakers, we have to rely on our own data based on our own patients. If patient scores are high then we continue as is, but if scores are less than an acceptable standard then we have to make some analysis of what needs to be done to improve scores.

-

Accountability and value creation through transparency

- If you have an objective patient-centered outcome approach you will be able to differentiate yourself form others in the value chain to payers, employers, and patients in an objective manner.

-

Improved quality

- Because O&P does not have a well-defined standard of care, fragmentation exists by region, within an organization, and within an individual office leading some patients to be under served, over served, or not served at all. An effective evidence data collection methodology can help improve the quality of care because clinicians have access to the results of their previous care decisions.

-

Improved functional outcomes

- The old saying goes, you cannot manage what you do not measure. If we measure the effectiveness of our clinical treatment decisions in a definable and repeatable way, we can continually make changes to our clinical protocols to improve the human impact we have on our patients.

A number of O&P companies have asked why the contracts presented to O&P are at discounts to the Medicare fee schedule whereas many others in healthcare are at some percent above Medicare rates.

The answer quite simply is we (O&P) have not given payers any evidence for an alternative payment model (APM). If you begin to measure the effectiveness of your current prescriptive habits by your patients actual functional and quality-of-life status and can demonstrate how you have iterated your processes to improve your scores, you can eventually go to the narrow network panels to request to be part of the “Club” and argue for different payment methodologies. One of the growing trends in Employer Sponsored Plans will be network cost containment. National price transparency efforts and those in O&P who can demonstrate both cost control and quality will prevail. Also, by understanding your data and acting upon what you have learned you can assume some risk with payers based on knowledge and can drive these alternative payment models. Conversely, if you do not have any data on your patient’s actual vs. potential performance, any payment discussions can only be based on price driven by the payer; a slippery slope indeed.

If you want to be part of the “Club,” Vanguard Metrics and Analytics has developed a program making it affordable and easy for you to participate. Your participation can make a difference!